Every Quote Is Free & Confidential

Every Quote Is Free & Confidential  Should I Fix My Mortgage?Competitive Fixed Rates From Mutliple Lenders |

|

A mortgage will be one of the biggest financial commitments you will ever take on and making the right decisions when it comes down to the mortgage you choose can be crucial. With anything in life it never hurts to get some expert advice and with a quarter of a century`s experience representing UK consumers in the mortgage sector, First Choice Finance is perfectly placed to help you answer any questions you might have. Whether that question is; should I fix my mortgage? Or simply can I get a mortgage? Or even how do I get a mortgage and how much will it cost? Our understanding advisers are here to listen and guide you through the mortgage maze. To help you address these all important questions call the our in house finance team on or complete the form at the top right of this page. Don`t worry we will not carry out a credit search from this from. In the meantime, read on to explore your options when it comes to fixing a mortgage rate.

A mortgage will be one of the biggest financial commitments you will ever take on and making the right decisions when it comes down to the mortgage you choose can be crucial. With anything in life it never hurts to get some expert advice and with a quarter of a century`s experience representing UK consumers in the mortgage sector, First Choice Finance is perfectly placed to help you answer any questions you might have. Whether that question is; should I fix my mortgage? Or simply can I get a mortgage? Or even how do I get a mortgage and how much will it cost? Our understanding advisers are here to listen and guide you through the mortgage maze. To help you address these all important questions call the our in house finance team on or complete the form at the top right of this page. Don`t worry we will not carry out a credit search from this from. In the meantime, read on to explore your options when it comes to fixing a mortgage rate.How Can I Fix My Mortgage?

A fixed rate mortgage is defined as a `mortgage type that guarantees your mortgage monthly repayments over a set period of time`. Effectively locking them at a certain price so that you know exactly how much your mortgage is going to cost you each month. These rates are typically fixed for a period of two, three, four or even five years but this can vary and sometimes longer term fixed rate mortgages are available, your adviser will explore those available to us for you.

A fixed rate mortgage is defined as a `mortgage type that guarantees your mortgage monthly repayments over a set period of time`. Effectively locking them at a certain price so that you know exactly how much your mortgage is going to cost you each month. These rates are typically fixed for a period of two, three, four or even five years but this can vary and sometimes longer term fixed rate mortgages are available, your adviser will explore those available to us for you.If you are considering the question; should I fix my mortgage? You are likely to be asking yourself exactly how you go about doing it. An efficient and hassle free option is coming to an experienced advice providing mortgage broker (described as an `intermediary`) like ourselves. We take on the burden of sourcing and arranging your mortgage from application to completion, supporting you all the way through leaving you only having to concern yourself with the key documents to read , digest and sign and to plan on how you are going to use the money once it is in your bank.

The Benefits And Drawbacks Of A Fixed Rate

Like anything in life weighing up the pros and cons is the best way forward. Should I fix my mortgage? This question is no different. We can help you in putting your best foot forward by considering some advantages and disadvantages of a fixed rate mortgage:- The Good Points

- A fixed rate can give you piece of mind knowing that you only have to make a certain payment each month and this isn`t going to change.

- With a fixed rate mortgage you can budget your monthly outgoings, giving you a better idea of what you can spend on the daily costs of living each month.

- If interest rates rise you will not have to pay any extra on your mortgage payment each month because it is fixed at the agreed amount.

- Negative Things To Consider

- With a fixed rate mortgage your payments are fixed for a set period of time. This means that if the interest rates drop your payment will stay the same and you won`t benefit from the decrease.

- There could be costs involved with fixing your mortgage, sometimes lenders will charge an arrangement fee to secure the product and there may be cheaper variable or tracker mortgages available which actually do not surpass your chosen fixed rate for the duration of your fixed term

- There will be early repayment charges if you choose to pull out of the fixed rate before the end of the discounted period, these can be significant and should be properly considered in your decision making process.

Is there A Cost For Fixing My Mortgage?

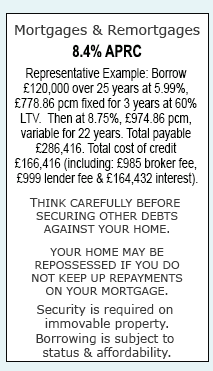

If you are looking into the possibility of whether you should fix your mortgage it is also worth considering any potential costs involved. Simply contact head office on a BT landline free phone number 0800 298 3000 (landline) or using 0333 003 1505 (included in mobile plan minutes) and our advisers will establish if we can help and then offer to furnish you with a free fixed mortgage or remortgage quote with absolutely no obligation to proceed. This quote will factor in any costs that might be involved with fixing your mortgage so that you know exactly how much or how little it might cost you. Letting you make a decision in your own time, with all of the information to hand.Alternatives To A Fixed Rate Mortgage

If you have considered the question should I fix my mortgage? You may have come to realise that it isn`t necessarily the best option for you going forward. This could be for a number of reasons, namely that you do not think variable mortgage rates will move up high enough during the fixed rate period to make it worthwhile or you want to benefit from any possible drops in individual lenders interest rate to win more business. For whatever reason a fix rate might not be for you, we will have other options available. Tracker rate mortgages which run at a fixed amount above or below a stated reference interest rate, standard variable rate mortgages, discounted rate mortgages and many more, we will endeavour to help you address your needs and provide you with an option suitable for your individual circumstances. Even if you just want to explore your options and soak up the knowledge of a mortgage adviser, then we are happy to listen to your specific goals and impart our thoughts to you.Mortgages & Remortgages |

Late repayment can cause you serious money problems. For help, go to moneyhelper.org.uk

Established In 1988. Company Registration Number 2316399. Authorised & Regulated By The Financial Conduct Authority (FCA). Firm Reference Number 302981. Mortgages & Homeowner Secured Loans Are Secured On Your Home. We Advice Upon & Arrange Mortgages & Loans. We Are Not A Lender.

First Choice Finance is a trading style of First Choice Funding Limited of 54, Wybersley Road, High Lane, Stockport, SK6 8HB. Copyright protected.